Since AfCFTA trading started in 2021, there has been more trade between countries, some new investments, and growth in sectors such as automotive manufacturing, pharmaceuticals, and digital services. Some jobs have been created, and a few countries expanded social protections. However, progress varies. Trade unions are raising crucial questions: Who benefits from this trade? Are the gains being fairly distributed? Are workers seeing the gains? What structural issues need to change to ensure fair trade?

This article draws on an impact review of the AfCFTA’s post-launch phase (2021–2025) conducted by the Africa Labour Research and Education Institute, alongside insights shared at the June 2025 trade union convening on AfCFTA, hosted by ITUC-Africa and the Labour Research Service in Kenya.

The African Continental Free Trade Agreement (AfCFTA)

The AfCFTA is the world’s largest free trade area, bringing together 54 countries, a population of 1.3 billion, and a combined GDP of US$3.4 trillion. The AfCFTA promises market access, industrial diversification, and job creation.

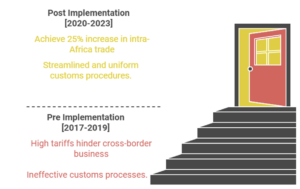

Before AfCFTA’s launch, intra-African trade was just 16% of total trade, compared to 59% in Asia and 68% in Europe. This was largely due to non-tariff barriers, poor logistics infrastructure, multiple currencies, and fragmented standards. For example, the average customs dwell time was 126 hours, and logistics costs were nearly double the global average.

Since its adoption in 2018 and operational launch in 2021, the AfCFTA has been implemented in phases. Phase I covers trade in goods and services, and dispute settlement protocols. Phase II extends to investment, competition, intellectual property, digital trade, and women and youth protocols. Regional Economic Communities are the building blocks of implementation, and the Guided Trade Initiative, launched in 2022, has piloted actual trade under AfCFTA rules in 35 countries.

Regional Economic Communities

A key feature of the agreement is tariff liberalisation: Ninety per cent of tariff lines are to be liberalised over 5 to 10 years, with a further 7% considered “sensitive” products and liberalised over 10 to 13 years, and a 3% cap on “excluded” tariff lines. As of October 2024, 37 member states had submitted their tariff schedules.

Supporting operational instruments have been rolled out, including the AfCFTA e-Tariff Book, a Rules of Origin manual, the Pan-African Payment and Settlement System, a non‑tariff barrier reporting and resolution platform, and trade facilitation dashboards linking to corridor management systems.

Post implementation impact

Trade growth

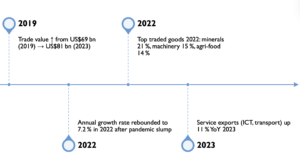

Intra-African trade grew from US$69 billion in 2019 to US$81 billion in 2023. After the pandemic-induced dip, the growth rate rebounded to 7.2% in 2022. Top traded goods in 2022 included minerals (21%), machinery (15%), and agri-food products (14%). Service exports, particularly in ICT and transport, grew 11% year-on-year in 2023.

Trade facilitation gains

Customs clearance times along key corridors, such as Tema–Abidjan, have dropped from 12 hours to 9.5 hours. More than half of the 220 non-tariff barrier complaints logged through AfCFTA’s platform were resolved, with an average resolution time of 39 days. Logistics costs fell in select corridors (-9 % and –5 % for road freight and maritime, respectively), and the Pan-African Payment and Settlement System pilots saved between US$5 and US$8 million in foreign exchange conversion fees in two years.

Macroeconomic contribution

AfCFTA-linked trade added an estimated 0.5 percentage points to Africa’s Growth Domestic Product (GDP) growth in 2022. The United Nations Economic Commission for Africa projects a cumulative GDP gain of US$450 billion by 2035 due to the agreement. Foreign direct investment inflows into AfCFTA member states rose by 17% between 2021 and 2023. There are signs of export diversification in Kenya and Morocco.

Regional disparities and barriers

The benefits are not evenly spread. Targeted support is required for underperforming regions.

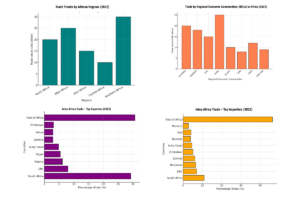

- Southern African Development Community leads with 35 % of intra‑African trade value, the Economic Community of West African States (24 %) and the Common Market for Eastern and Southern Africa (18 %).

- Central Africa contributes just 6 % owing to infrastructure and governance gaps.

- Trade within Regional Economic Communities (REC) grew faster (+9 %) than cross‑REC flows (+5 %) in 2023.

Industrial development signals

Ghana and Kenya attracted more than US$600 million in new investments in automotive assembly. Pharmaceutical hubs in Nigeria and Egypt have scaled fill-to-finish vaccine manufacturing. Meanwhile, the digital economy is expanding rapidly, with e-commerce turnover rising by 24% and mobile money transactions growing by 31% between 2021 and 2023. The demand for Fourth Industrial Revolution skills, including robotics, artificial intelligence, and blockchain, is growing.

Labour market outcomes

The agreement has been linked to the creation of 2.3 million net new formal and informal jobs across 25 African countries between 2021 and 2024, with youth employment shares rising by 1.8 percentage points in countries participating in the Guided Trade Initiative. Seven countries have introduced new wage-setting frameworks tied to productivity. However, skills shortages remain in critical sectors, including logistics and digital services.

Social protection and labour rights

Trade-linked fiscal space enabled Rwanda and Senegal to expand health insurance to 68 % and 62 % of the population, respectively. Still, worker rights remain precarious. The 2024 ITUC Rights Index found that 11 countries offered no guarantees of fundamental labour rights. Trade unions are calling for stronger, enforceable labour and social clauses in AfCFTA annexes and national implementation plans.

Projections for 2035

Intra-African trade could double to represent one-third of the continent’s total trade. Africa’s middle class is projected to grow to 390 million people. Digital trade is expected to surpass US$180 billion, with fintech and e-logistics as major drivers. Enforceable labour standards could deliver a net welfare gain of US$57 billion.

Trade union actions

Secure union representation on National Implementation Committees and REC trade structures.

Negotiate sectoral wage floors tied to productivity and value addition.

Monitor the quality-of-work impacts of non-tariff barrier resolution and trade facilitation.

Champion gender-responsive trade and integrate youth-led enterprises into continental value chains.

Advocate for climate-resilient trade policies and accessible just transition finance mechanisms.

Summary policy recommendations

- Accelerate infrastructure development (multimodal transport, energy, digital) through blended finance.

- Embed enforceable labour and social protection clauses in AfCFTA protocols and national development plans.

- Scale the Pan-African Payment and Settlement System pilot and harmonise cross-border payment regulations to reduce forex costs.

- Strengthen REC and National Implementation Committee coordination, supported by real-time dashboards for non-tariff barrier monitoring.

- Invest in green skills and climate-just transition strategies aligned with trade and industrial development.

_____________________________________

Source of graphs: ALREI (2025) ‘An Impact Analysis of the African Continental Free Trade Area (AfCFTA) in its Post-Implementation Phase (2021-2025): A Trade Union Lens‘.

A presentation on the impact analysis study to trade unions.

Trade, Employment and Trade Unions in Africa: Some Policy Options.

Key trade union demands for the AfCFTA.

Nelly Nyagah

Nelly Nyagah is the Head of Communications at Labour Research Service.